Fletcher Building releases its quarterly update of key product sales volumes for the March quarter of the 2026 financial year (Q3 FY26).

Andrew Reding, Managing Director and Chief Executive Officer, said: “Quarterly volumes for the March quarter continued to show early signs of improvement across the portfolio, with the important caveat that this quarter largely preceded the current geopolitical escalation. Light Building Products benefited from improved Alterations & Additions (A&A) activity in New Zealand and a broad-based uplift in Australia. Heavy Building Materials remains subdued overall, although we’re seeing pockets of activity tied to project work. Distribution, particularly frame & truss, continues to show steady improvement as underlying demand gradually returns. As was the case in prior quarters, trading conditions remained competitive, with ongoing margin pressure and compression continuing across business units and most notably in the Distribution division, Firth and the Steel business units.”

Divisional Volumes

-

Light Building Products volumes continued a positive trend and are generally up versus Q2 and prior corresponding period (pcp). Volume growth was seen in Waipapa Pine and Iplex NZ, with both up versus Q2 (1.4% and 5% respectively) and versus pcp (16.5% and 15.9% respectively) with Waipapa Pine benefitting from onboarding of two key industrial clients. In Australia, volumes have generally improved relative to both Q2 and pcp, with Laminex AU, Iplex AU and Fletcher Insulation delivering positive performance as momentum continued across all states.

-

Heavy Building Materials performance remained mixed. Winstone Aggregates volumes declined -0.9% versus Q2 and -10.4% versus pcp. However, there were positive movements in aggregates and concrete pipes in Q3 with the start of new major projects. Humes volumes were also down -0.7% and -4.8% on Q2 and pcp respectively. Firth and Golden Bay volumes had minor declines on both Q2 and pcp. Steel volumes were uneven, despite positive developments in Dimond and ColorCote.

-

Distribution Frame & Truss volumes continued to be positive, up 3.4% versus Q2 and 6.6% versus pcp, as increasing building consents lifted overall market activity, as well as ongoing improvement in market share.

-

Residential took 93 residential and apartment units to profit in Q3, including 7 bulk lot sales. Excluding bulk lots, underlying take to profit (TTP) was 21 units lower than Q2 in FY26, reflecting ongoing challenging market conditions. TTP was 22 units lower vs pcp, largely driven by the phasing of three long-standing sold-out developments.

The majority of Q3 FY26 volume data predates recent global geopolitical developments, with escalation occurring only in the final weeks of the period.

Post-quarter impact of Middle East conflict

The escalation of the Middle East conflict has heightened global geopolitical risk, particularly in energy markets, key shipping routes, and the pricing and availability of critical inputs. While Fletcher Building has no direct operations in Iran, the Group is exposed indirectly through supply chains, freight routes, energy costs, and broader macroeconomic impacts on construction demand across Australasia.

Business Units have responded promptly in a measured manner, with actions focused on maintaining continuity of supply, protecting margins and cash flow, and preserving strategic optionality under a range of downside scenarios.

Key areas of risk across the Group

-

Direct supply chain risk: The most immediate exposure is in plastics (i.e., resins), with Iplex NZ and AU most impacted. Urea used in Laminex AU, Laminex NZ and Fletcher Insulation products is also exposed. Short-term supply has been secured, with mitigation actions underway to diversify sourcing and manage potential constraints.

-

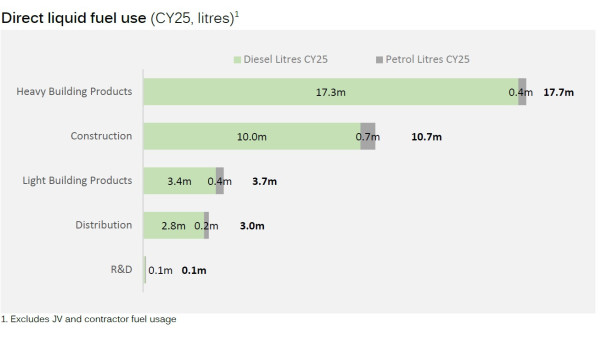

Fuel exposure: Fuel remains a material cost driver, with diesel representing the majority of consumption across the Group. While the price increases to date are significant, the impacts are being partly mitigated through bulk purchasing, hedging and pass-through pricing mechanisms. Unhedged, a 10c increase in diesel prices results in an incremental cost of approximately $3.4m p.a. at a Group level ($2.4m p.a. excluding Construction), while a 10c increase in petrol prices equates to approximately $0.2m p.a incremental cost at a Group level.

The Group consumes nearly 36 million litres of fuel annually, with diesel accounting for 94% of total usage. The Heavy Building Materials division represents over half of total consumption, with the Construction division accounting for nearly a third. -

Pricing and customer response: Price increases across divisions range from modest (~1–5%) to more significant in plastics (up to 36%) and include fuel-linked surcharges, reflecting input cost pressures. These have been broadly in line with wider industry responses. Early signs of demand softening are emerging, particularly through some project delays.

-

People impact: Direct impacts on employees have been limited to date, with anecdotal feedback on increased commuting costs, some requests for greater WFH flexibility, and references to fuel-driven cost-of-living pressures in union discussions. Activity has primarily focused on planning, with expectations that workforce impacts may increase if conditions escalate.